Tracking net worth in Google Sheets automatically means building a system where the components of your net worth that change most frequently, your bank account balances and transaction-driven liability balances, update themselves without any manual work from you. The components that change less frequently, investment portfolio values and property estimates, get updated periodically on a schedule you control. The result is a net worth tracker that is always close to current, always in a spreadsheet you own, and always available for the kind of longitudinal analysis that transforms a snapshot into a genuine financial trend.

Net worth is the single number that tells you whether your financial life is moving in the right direction. Investopedia defines it as total assets minus total liabilities. The definition is simple. Keeping the number accurate and current over time is where most approaches break down, because the manual effort required to update every component every month compounds quickly into a maintenance burden most people abandon within a few months of starting.

The system this guide builds eliminates the manual effort on the components that matter most. What remains is a quarterly review of the slower-moving inputs, which is a manageable commitment that most people will actually sustain.

Why Net Worth Tracking Usually Fails

Most people who try to track their net worth start with a spreadsheet. They enter their account balances, list their debts, subtract one from the other, and feel like the problem is solved. The number is accurate for about one week. Then accounts move, balances change, and the spreadsheet drifts further from reality every day it goes without an update.

The update problem is not a motivation problem. It is a friction problem. When updating your net worth tracker requires logging into five different bank portals, pulling balances from three credit cards, checking your mortgage balance, and entering all of it manually into a spreadsheet, the task takes 30 to 45 minutes. Most people do it once, feel virtuous, and do not do it again for six months. A net worth snapshot from six months ago is not a useful financial tool.

The automation question is therefore the most important design decision in building a net worth tracker. What can be made automatic, and what genuinely requires manual input? Getting that answer right is what separates a tracker you maintain from a tracker you abandon.

What Can Be Automated and What Cannot

Net worth is the sum of two categories: assets and liabilities. Within each category, some components update frequently and some update slowly. Automation should be applied where the update frequency is highest, because that is where manual effort compounds fastest.

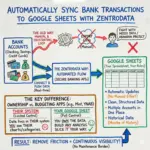

Assets that update frequently and can be automated: Checking account balances, savings account balances, and cash equivalents change with every transaction. These are the components where ZentroData’s automatic bank data sync delivers the most value. When your transaction data flows into Google Sheets automatically every day, your cash asset balances are always current without any manual input.

Assets that update slowly and require periodic manual input: Investment portfolio values, retirement account balances, and real estate estimates change in value continuously but do not require daily precision for net worth tracking purposes. A monthly or quarterly manual update is accurate enough to produce a meaningful net worth trend, and the infrequency makes the manual effort sustainable.

Liabilities that update frequently and can be automated: Credit card balances change with every transaction. Because ZentroData syncs credit card transactions alongside bank account transactions, the spending side of credit card liability is automatically reflected in your transaction data. For precise current balance tracking, a monthly manual balance entry is the practical approach, since ZentroData captures transactions but not the running balance directly.

Liabilities that update slowly and require periodic manual input: Mortgage balances, student loan balances, and car loan balances change slowly and on a predictable schedule. A monthly manual update drawn from your loan servicer’s statement is accurate enough and takes under five minutes per liability.

How to Track Net Worth in Google Sheets: Step by Step

Step 1: Set Up ZentroData for Automatic Transaction and Balance Data

Sign up at zentrodata.com, connect every bank account and credit card you own through the secure connection flow, link your Google account, and point ZentroData at your net worth tracking sheet. Set your sync schedule to daily and run your first manual sync immediately.

After the first sync, you have up to 90 days of transaction history from every connected account written into your transaction tab as clean, structured rows. This data powers two components of your net worth tracker: the cash flow analysis that shows how your net worth is changing month to month, and the running balance calculations you will build in the next steps to keep your cash asset values current.

Step 2: Build the Asset Tracker Tab

Create an asset tracker tab with the following sections:

Cash and bank accounts: One row per connected account. In the balance column, use a SUMIFS formula that calculates the running balance for each account from your ZentroData transaction data:

=SUMIFS(B:B,G:G,"Chase Checking")

Where column B is Amount and column G is the Account column ZentroData writes. This formula sums all transactions for that account across your entire transaction history. Add your opening balance for each account as a separate input cell and add it to the SUMIFS result. The sum of the opening balance plus all transaction amounts equals the current balance, updated automatically every time ZentroData syncs.

Investment accounts: One row per account. Enter the current value manually each month. Add a date column next to each balance so the tracker records when the value was last updated. A balance with a date that is three months old is meaningful context when you are reviewing the tracker.

Property and other assets: One row per asset. Enter estimated current values manually on a quarterly basis. Property values change slowly enough that a quarterly estimate is accurate for net worth trend purposes. Use a conservative estimate rather than an optimistic one. Net worth tracking is most useful when it reflects reality rather than best-case assumptions.

Step 3: Build the Liability Tracker Tab

Create a liability tracker tab with two sections:

Credit card balances: One row per card. Enter the current statement balance monthly. Credit card transaction data flows through ZentroData, which gives you complete visibility into spending, but the current carrying balance is best captured from the statement rather than calculated from transactions, since credits, payments, and timing all affect the actual balance.

Loan balances: One row per loan: mortgage, student loans, car loans, personal loans. Enter the current balance monthly from your loan servicer’s statement or online account. Add columns for the interest rate and minimum payment for each loan. These fields do not change often but are useful context when reviewing your liability picture.

For each liability, add a column that calculates the monthly change by subtracting the current balance from the prior month’s balance. This column shows paydown rate, which is one of the clearest indicators of whether your liability position is improving at the pace you expect.

Step 4: Build the Net Worth Summary Tab

Create a net worth summary tab that pulls from the asset and liability tracker tabs. The structure is straightforward:

Total assets: A SUM across every asset row in the asset tracker tab.

Total liabilities: A SUM across every liability row in the liability tracker tab.

Net worth: Total assets minus total liabilities.

Below the current snapshot, build a historical net worth table with one row per month and three columns: total assets, total liabilities, and net worth. Update this table monthly by entering the snapshot values from the current month. Over time, this table becomes the dataset for your net worth trend chart.

The historical table is the component that makes net worth tracking genuinely valuable. A single net worth number tells you where you stand. Twelve months of net worth numbers tell you whether you are moving toward or away from your goals, at what pace, and whether the pace is accelerating or decelerating. That trend is what no single snapshot can reveal.

Step 5: Build the Net Worth Trend Chart

Select your historical net worth table and insert a line chart with months on the x-axis and dollar amounts on the y-axis. Add three lines: one for total assets, one for total liabilities, and one for net worth.

The relationship between these three lines tells the story of your financial direction. A rising assets line with a flat or declining liabilities line means net worth is growing. A flat assets line with a rising liabilities line means net worth is being eroded. A net worth line that is rising but decelerating means growth is slowing, which warrants examination even when the direction is still positive.

Configure the chart to start from the earliest month in your historical table. The longer the time series, the more meaningful the trend. A six-month chart shows a recent pattern. A two-year chart shows whether the pattern is consistent or whether it reflects an unusual period.

Using ZentroData’s Spending Data to Understand Net Worth Changes

Net worth changes are driven by two forces: income coming in and spending going out. The difference between them is what either builds or erodes net worth each month. ZentroData’s transaction data, already in your sheet from the setup steps above, gives you the spending side of this equation automatically and completely.

Build a monthly cash flow summary on your net worth summary tab that shows total inflows, total outflows, and the net for each month. Use SUMIFS against the Amount column in your transaction tab to calculate total debits and total credits separately for each month:

Total outflows: =SUMIFS(B:B,A:A,">="&DATE(2026,3,1),A:A,"<"&DATE(2026,4,1),B:B,">"&0)

Total inflows: =SUMIFS(B:B,A:A,">="&DATE(2026,3,1),A:A,"<"&DATE(2026,4,1),B:B,"<"&0)

The net of these two numbers is your monthly cash flow. Positive means more came in than went out. Negative means the opposite. This number, tracked alongside your net worth trend, explains most of the month-to-month changes in your net worth line and identifies the periods where spending outpaced income before they compound into a pattern.

No budgeting app makes this connection between transaction-level spending data and net worth tracking visible in a spreadsheet you own. ZentroData’s automated data pipeline is what makes the spending side of this analysis current, complete, and automatic, which is the component that requires the most frequent updating and therefore produces the most maintenance burden when done manually.

Tips for Better Net Worth Tracking

- Update investment balances on the same day each month rather than whenever you remember. Consistency in the update date makes month-to-month comparisons meaningful because you are comparing balances at the same point in each month rather than at random intervals.

- Use conservative estimates for illiquid assets like real estate and personal property. Optimistic asset values inflate net worth in a way that feels good and misleads. A realistic estimate understates nothing and accurately reflects what you could actually convert to cash.

- Track the number of months of living expenses your liquid assets represent alongside the raw net worth number. Liquid net worth, the portion of assets you could access within 30 days, is a more immediately useful number than total net worth for most financial decisions.

- Do not include the value of depreciating assets like cars unless they represent a significant portion of your total assets. A car loses value every month and tracking it as an asset creates a false sense of stability in net worth when the asset is actually declining.

- Review your liability paydown rates quarterly and compare them to your loan amortization schedules. If a loan balance is declining more slowly than the amortization schedule predicts, something has gone wrong with your payments and catching it early matters.

- Connect every account to ZentroData, including accounts you rarely think of as significant. Small savings accounts, secondary checking accounts, and accounts linked to infrequently used credit cards all contribute to the complete picture. Omitting them understates assets and potentially understates liabilities.

- Build a separate net worth projection tab that extends your current trend forward six and twelve months based on your average monthly cash flow. A projection built on real historical data is a useful planning tool. A projection built on what you hope to do is a wish list.

Track Net Worth in Google Sheets: Approaches Compared

| Approach | Cash Data Automation | Multi-Account | Spending Integration | Data Ownership | Trend Tracking |

|---|---|---|---|---|---|

| ZentroData + Google Sheets | Full | Yes | Full | Complete | Unlimited |

| Manual spreadsheet updates | None | Yes | Manual only | Complete | Manual only |

| Budgeting app net worth views | Partial | Yes | Limited | None | Fixed reports |

| Dedicated net worth apps | Partial | Yes | Limited | None | Fixed reports |

| Bank app balance views | One institution | No | None | None | None |

The pattern is consistent with every comparison in this space. Dedicated net worth apps and budgeting apps with net worth features automate portions of the data collection but lock the analysis inside their own closed systems. Manual approaches give you complete flexibility and data ownership but fail under the maintenance burden over time. ZentroData combined with Google Sheets delivers full cash data automation, complete spending integration, and complete data ownership simultaneously, which is why no other approach produces a net worth tracker that is both accurate and sustainable long-term.

Frequently Asked Questions About Tracking Net Worth in Google Sheets

Q: How often should I update my net worth tracker?

A: The cash and bank account components update automatically every day via ZentroData. Investment balances and property values should be updated manually once a month. Loan balances update monthly from your statements. Recording a historical snapshot of total net worth once a month, on the same date each month, builds the trend data that makes the tracker genuinely useful over time. The monthly snapshot takes under ten minutes once the tracker is set up correctly.

Q: Should I include my home value as an asset in my net worth tracker

A: Yes, with caveats. Your home is a real asset that contributes to net worth, but its value is an estimate rather than a market price until you sell. Use a conservative estimate based on recent comparable sales in your area rather than an optimistic projection. Also track the mortgage balance as a corresponding liability. The equity in your home, the difference between estimated value and outstanding mortgage balance, is the accurate net worth contribution of your property.

Q: How does ZentroData help with net worth tracking specifically?

A: ZentroData automates the components of net worth tracking that require the most frequent updating: cash account balances and transaction data. By syncing every transaction from every connected bank account and credit card into your Google Sheet daily, ZentroData keeps the cash side of your net worth tracker current without manual effort. It also provides the spending data that explains why your net worth changed each month, connecting transaction-level behavior to the net worth trend in a single spreadsheet you own. No other tool makes both the asset balance data and the spending analysis available together in a format you control.

Q: What is the difference between net worth and liquid net worth?

A: Net worth is total assets minus total liabilities, including all asset types regardless of how quickly they can be converted to cash. Liquid net worth counts only assets you could access within 30 days: cash, checking accounts, savings accounts, and publicly traded investments. It excludes retirement accounts with early withdrawal penalties, real estate, and illiquid investments. Liquid net worth is the more conservative and more immediately useful number for financial planning because it reflects what you could actually deploy in an emergency or an opportunity.

Q: How do I handle retirement accounts like a 401k in my net worth tracker?

A: Include retirement accounts as assets in your tracker at their current balance, updated manually each month. They are real assets that belong in your net worth calculation even though they cannot be accessed without penalty before retirement age. Track them separately from liquid assets and label them clearly so your net worth summary distinguishes between what you can access immediately and what is long-term. The distinction between total net worth and liquid net worth becomes important context when the retirement account balance represents a significant portion of total assets.

Q: Can I use this tracker to set and monitor a net worth growth target?

A: Yes. Add a target net worth line to your trend chart, calculated from your starting net worth plus a monthly growth amount that reflects your savings and investment goals. The gap between your actual net worth line and your target line is your progress indicator. When the gap narrows, you are on track or ahead. When it widens, something in your cash flow or investment performance is below the pace the target assumes. The target line turns the net worth chart from a record of the past into a navigation tool for the future.

The Number That Tells the Whole Story

Income tells you what you earn. Spending tells you what you consume. Net worth tells you what you are building. It is the number that accounts for everything simultaneously: every dollar earned, every dollar spent, every debt paid down, and every asset accumulated. No single financial metric contains more signal about the direction of your financial life.

The reason most people do not track net worth consistently is not that they do not care about the number. It is that keeping it accurate has historically required more manual effort than most people will sustain indefinitely. ZentroData eliminates the manual effort on the components that update most frequently, reducing the ongoing work to a monthly ten-minute review that almost anyone will actually do.

That combination, accurate data, automatic updates on the components that change most often, and a spreadsheet you own permanently, is what makes the difference between a net worth tracker you build once and a net worth tracker you actually use. If you want to see what your own numbers look like in a system like this, ZentroData’s free trial at zentrodata.com is where to start.